Employer based insurance is failing. It doesn’t work for employers, many of whom can’t afford to provide coverage, particularly those with lower income employees. And it doesn’t work for the employee who either has no insurance or has to spend a significant proportion of income to buy coverage.

McKinsey Quarterly notes that :

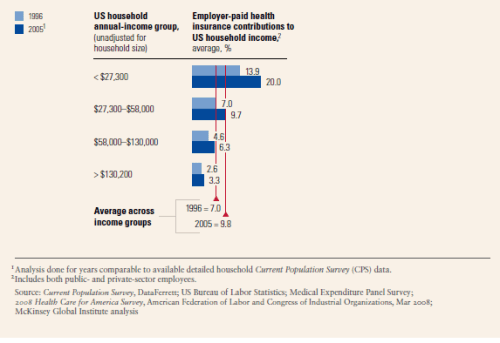

“In 2005, employer-paid health benefits covered 22 percent of households in the bottom-income group, contrasted with 56 percent of the lower-middle, 81 percent of the upper-middle, and 89 percent of the top income group”

To understand the magnitude of costs relative to income:

You will note for those earning under $27,000 dollars/year, health insurance costs are in the range of 20% of income, while for those earning over 130,000/year it’s just 3.3%.

Meanwhile Ramesh Ponnunu (of the National Review) in an OP-ED, advocated a move away from employer provided health insurance. Medicynical note: Can’t argue with that as I believe the employer based insurance system has failed.

His approach, however, would allow employers to drop health insurance and provide a tax credit to the employee to buy insurance on the private, individual market. He argued that this will bring market forces to bear on health care costs.

His plan discounts the high cost of insuring those with illness, that of course is the whole point of health insurance saying vaguely that they would be provided subsidies to buy coverage. He also neglects the issue of below average income people (after all that is 50% of the population) and the high cost of health insurance, relative to income.

His tax credits, as I understand it, will provide a decrease in the amount of taxes paid. But it won’t provide relief for a significant part of our population. For example, families and individuals with $27,000 or less income have no tax liability (see here).

We can do better than this.

Powered by Zoundry Raven